Current Market Volatility

While a sharp decline in stock prices is unnerving, panic is not an investment strategy

- Plummeting stock prices on Monday were associated with oil-price volatility on top of an already nervous market concerned about the Coronavirus outbreak

- We believe an economic bounce back is probable later this year

- Additional coordinated global fiscal and monetary policies are increasingly likely

- The global financial system is much stronger and more resilient than thirteen years ago

- Stock market declines sometimes have silver linings: in this case, lower prices, particularly in the energy sector, and very attractive dividend yields versus bond yields

By Thomas J. Connelly, CFA, CFP®

President and Chief Investment Officer, Versant Capital Management, Inc.

Stock markets across the world declined sharply yesterday, with some markets putting in their largest daily declines since December 2008. The S&P 500 dropped 7.6 percent, while market declines in the rest of the world ranged from 3.1 percent to more than 15 percent. It happened despite a surprise 0.50 percent decline in the Federal funds rate last week to a target range of 1.0 to 1.25 percent. What started as selling from automated systematic strategies and option hedging in late February has morphed into market-wide selling. Fearful investors are putting buying pressure on government bond markets, driving U.S. interest rates to further historic lows in the process. Yesterday Treasury yields finished below 1 percent across the yield curve, leaving investors, savers and retirees in a tight spot.

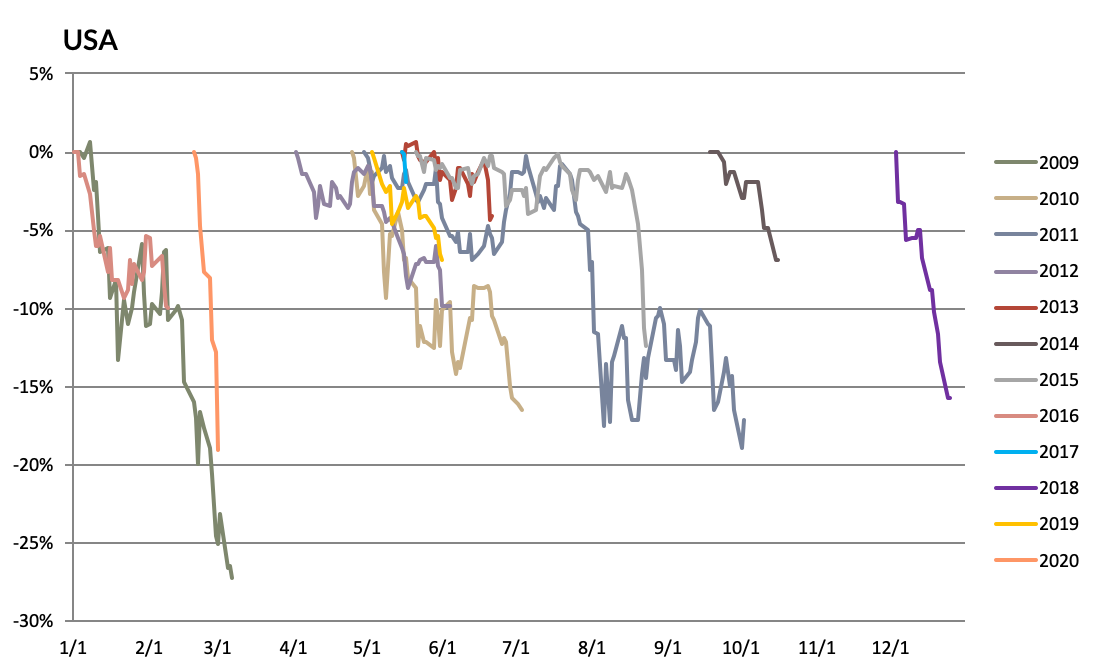

The chart below illustrates the most significant intra-year declines over the last twelve years, beginning in 2009. For 2020, the U.S. stock market is approaching bear market levels, generally defined as a drop of 20 percent or more. Returns during the 2020 decline are slightly better in the aggregate for the rest of the developed world and emerging markets. Similar declines are evident in 2009, 2010, 2011, 2012, and the end of 2018.

What is different about 2020 is the speed at which this market decline has hit. But what is not that unusual is that sizable decline happened in 2020. Market drops greater than -15 percent occurred in four of the previous eleven years.

Yearly Declines in MSCI Indices, 2009-2020

(Updated through March 9, 2020)

Source: MSCI, Morningstar

Yesterday’s selling is associated with continuing fears around the coronavirus and the Saudi oil company Aramco’s announcement last weekend to slash selling prices. It caused oil prices to drop 24 percent to little more than $32 a barrel (bbl), down 50 percent from its peak on January 6. The backdrop is one of oversupply combined with an unexpected drop in demand due to coronavirus-related economic retrenchment . Aramco’s announcement came after Russia declined to participate in an OPEC proposal to limit production to raise or stabilize oil production due to lower demand generated by the coronavirus epidemic.

In addition to airline and other travel and transportation-related stocks, oil companies and banks were hit especially hard yesterday. It is worth noting that the only fields that can operate without losing money at $32/bbl are in the middle east. Shale producers need $47 to $54/bbl to break even, while most other producers need $41 to $60/bbl. Oil sands and arctic producers need north of $70/bbl. The oil price shock is well below the cost of production for most of the world’s oil producers, and well below the price needed to balance any producers’ government books. This low oil price is not sustainable – it’s more of a buying opportunity for assets that are priced for a fire-sale.

Versant Capital Management’s opinion is that the coronavirus epidemic will be a temporary economic dislocation, as were all the other epidemics that preceded it. While we cannot be sure of the extent of the epidemic or its immediate economic consequences, we do know that the coronavirus will end, just as the SARS, MERS, H1N1, and Zika epidemics all ended, and did not result in lasting economic or market damage. Before the coronavirus epidemic, U.S. economic activity was still relatively strong, and Europe and parts of Asia were beginning to show some strength. Material interest rate reductions by central banks and fiscal stimulus that is doubtlessly coming tends to be somewhat sticky, increasing the possibility of a melt-up in asset prices post-epidemic.

The potential human and economic impact that the coronavirus epidemic may cause is not without grave concern. Economists are continually revising global growth estimates for 2020 as the epidemic spreads from China to the rest of the world. The positive news here is that in China, the rate of increase is decelerating, and economic and social activity is beginning to recover. New diagnoses appear to be declining in South Korea, as well.

Yesterday Italy restricted activity throughout the country, and new cases are accelerating in the U.S., in the rest of Europe, and are popping up in new countries daily. The danger is far from over. We don’t know what the economic impact will be in countries experiencing the early stages of the coronavirus epidemic, and there is the possibility that in the aggregate, the cumulative economic damage will transform into a longer-lasting and more damaging global recession.

There are some positive forces building that will counteract the fear of the coronavirus and its impact on the global economy:

- Interest rate reductions by central banks

- Yet-to-be-announced fiscal stimulus

- Consumer windfall for lower energy prices

- Lower materials prices

- Lower travel costs and some forms of entertainment

- Mortgage refinance opportunities

- Other debt and reduced financing costs resulting in more discretionary income for consumers

The majority of economic consequences coming from coronavirus fear are deflationary, making a coordinated response involving both monetary and fiscal stimulus necessary. Monetary policy in the form of interest rate reductions is not enough to get resources into the hands of consumers to increase spending. Only fiscal policy can do that. Plans about what the EU and the U.S. are going to do should be out soon, perhaps as early as Thursday.

Good news? We are not looking at another 2007-2009 collapse

The global financial system is very different from what it was in 2007. Banks used to take on most of lending to consumers and corporate buyouts and were the prime channel for translating financial stress in the credit markets back into the general economy. Banks in the developed world, except for Italy and Greece, have much higher capital cushions, lower levels of leverage, much more liquidity, and more stable and diverse and stable funding sources today.

Today, many types of risky lending are dispersed outside of the banking system. Risky debt holders are diverse, spreading out the impact of negative credit shocks, rather than concentrating them in the banking system. In the private sector, economic growth has been powered by income growth rather than increasing debt. Growth in corporate lending — particularly in the private equity financing leveraged loan space — is now generally done outside the banking system. Globally, banks now undergo periodic regulatory stress tests, which has increased oversight and put checks and balances in place.

Shadow banks (lightly regulated, non-bank lenders) contributed to pre-crisis leverage excesses. Securities lending activities have dropped from a peak of more than 15 percent of GDP to less than 5 percent today, and asset-backed security issuance has declined from almost 30 percent of securities lending activity to around 5 percent. The multi-trillion dollar money market fund business faced strict regulations and was forced to prohibit leverage for financial and non-financial lenders.

The vast imbalances between countries in terms of trade deficits and surpluses, budget deficits, and large capital account imbalances are greatly diminished today (except in the U.S.), relative to pre-crisis years.

Trading volume across major asset classes has almost doubled in the aggregate from the same time last year, and there have been no significant breakdowns in market liquidity or jumps in trading costs. Throughout the coronavirus epidemic, trading has been functioning well and does not seem to be contributing to market volatility. Currently, there are no large pricing dislocations in ETFs that hold less liquid underlying assets. It’s difficult today for banks or other financial institutions to leverage illiquid investments in the Repo markets due to regulatory treatment. The swaps market used to be a wild west of customized contracts between institutions. Now they’re primarily standardized contracts that clear on organized exchanges, greatly reducing counterparty risk and giving regulators a much better idea of the size and scope of activity.

Simply put, the meaningful regulatory and structural changes that have been put in place since the Great Financial Crisis suggest that the probability of a liquidity or solvency crisis similar to what happened in 2007 to 2009 is not likely. The GFC was the previous war. The next war will be fought on different ground and with different weapons.

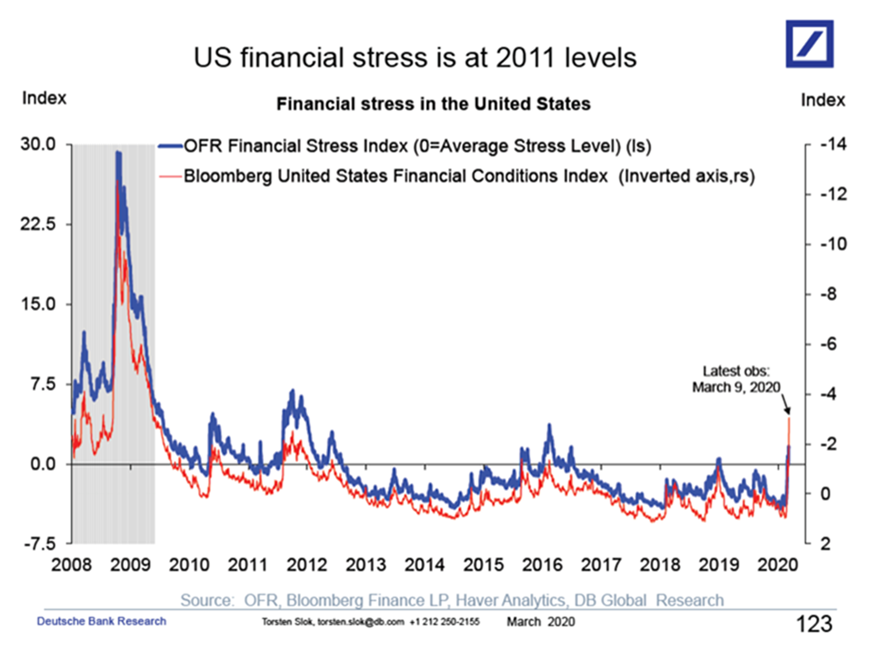

Measures of financial distress elevated recently to levels last seen during the European banking crisis on 2011, but are nowhere near what we saw in 2008 and 2009.

Good news is that bad news makes for good prices

Case in point, the energy sector now trades with oil prices at a level that will not support most current production costs, much less the cost of replacing consumed resources, or supporting the fiscal needs or producers’ government spending needs. The sector has been in distress for much of the past five years, and the weight of the energy sector is now a third of its pre-GFC weight. Energy stock prices were further punished Monday and investors are treating oil company and service stocks as if they were radioactive. We view the traditional energy sector as a long-term buying opportunity.

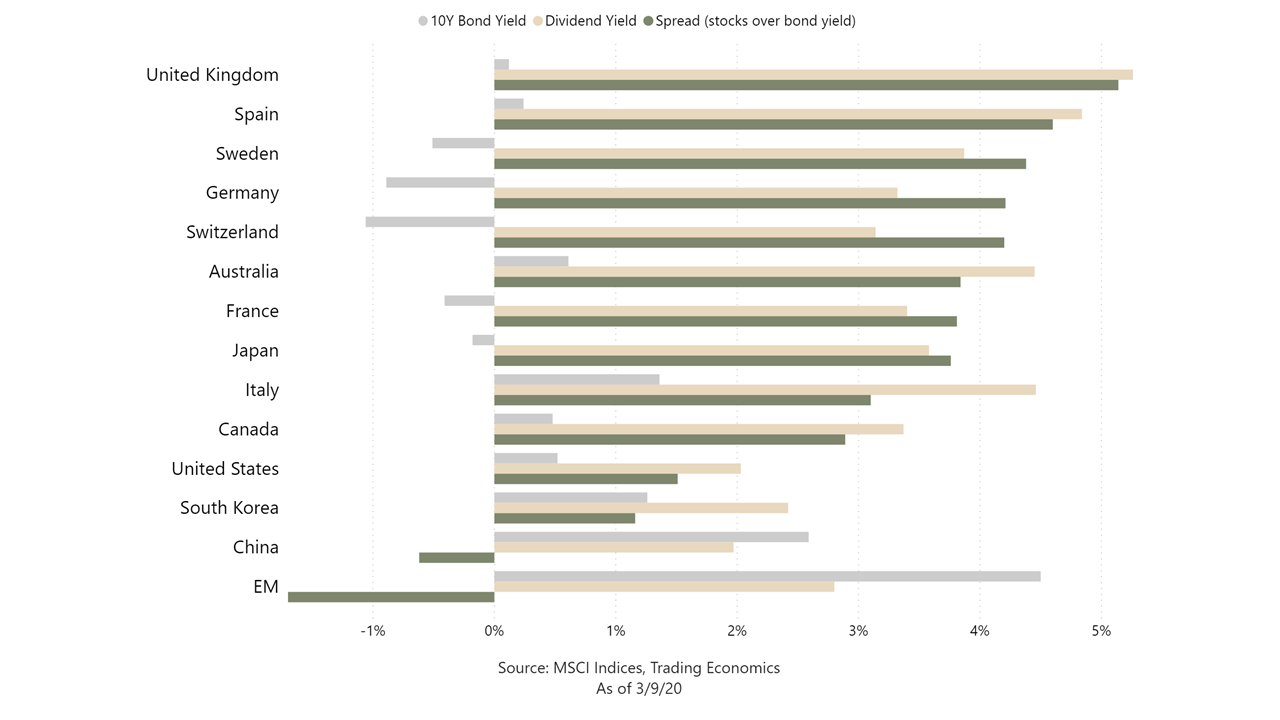

Government interest rates available to investors, savers, and retirees are currently below 1 percent in the U.S. Treasury market. In many European and Asian countries, government bond yields are lower or even negative as in Germany, Sweden, Switzerland, Japan, and France.

The differentials between stock market dividend yields and available government interest rates from recent stock market declines and interest rate reductions are astounding. A German investor can make 4 percent more in dividends from investing in the German stock market than in the Bund market (long term obligations of the German government that are auctioned off in the primary market). That doesn’t consider earnings growth (and thus dividend growth) that will occur over the investor’s time horizon.

The differentials between stock market dividend yields and available government interest rates from recent stock market declines and interest rate reductions are astounding. A German investor can make 4 percent more in dividends from investing in the German stock market than in the Bund market (long term obligations of the German government that are auctioned off in the primary market). That doesn’t consider earnings growth (and thus dividend growth) that will occur over the investor’s time horizon.

The biggest differentials are abroad, primarily in Europe. But in the U.S., the difference is still a healthy 1.4 percent. We haven’t seen differentials such as those abroad in the post-war period. In our view, either stocks are underpriced, or bonds are extremely overpriced due to fear. It’s not a time to sell stocks and go into more conservative assets.

If you have questions about your customized investment plan, please contact your Versant Capital Management wealth counselor.

Related

A Transformed Investor’s Reaction to Coronavirus

Dave Goetsch, Executive Producer of The Big Bang Theory, on why you should invest long-term

For investors, it can be easy to feel overwhelmed by the relentless stream of media noise

The Coronavirus and the Global Financial Markets

Disclosure: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Versant Capital Management, Inc.), or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from Versant Capital Management, Inc. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Versant Capital Management, Inc. is neither a law firm nor a certified public accounting firm and no portion of the article content should be construed as legal or accounting advice. If you are a Versant Capital Management, Inc. client, please remember to contact Versant Capital Management, Inc., in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Versant Capital Management, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.