Prepared by Brandon Yee CFA® and Thomas Connelly CFA®

Commentary

Commentary

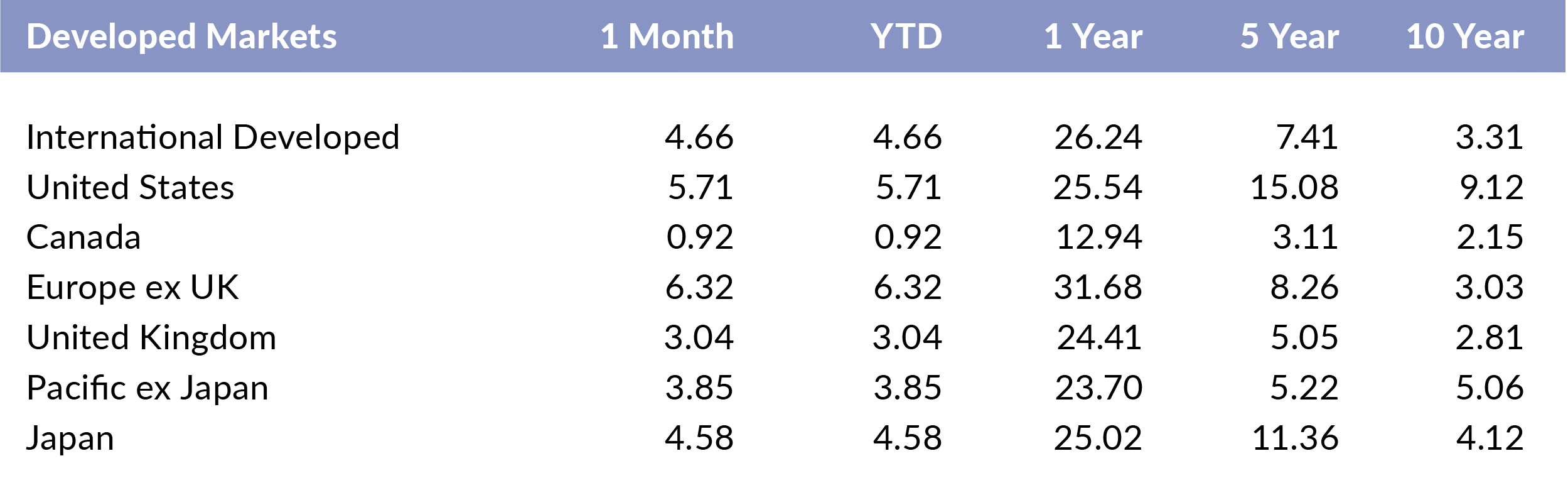

Developed Markets Off to Strong Start– In the month of January, developed markets recorded strong returns. Europe ex UK and the U.S. posted strong gains of 6.32% and 5.71%, respectively. Canada and the UK lagged other regions. The strong performance from 2017 has certainly carried over into 2018; however, care should be taken to avoid extrapolating these high returns.

Commentary

Commentary

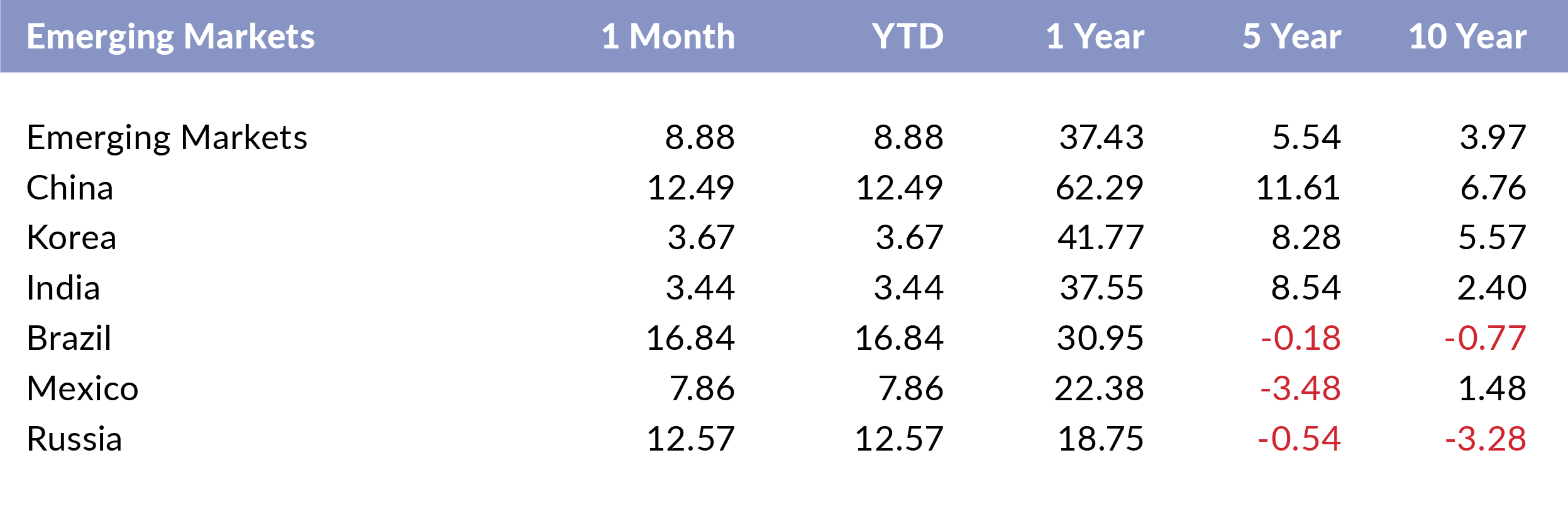

Emerging Markets Deliver Sizable Returns – The broader emerging markets were up 8.88% in January. Brazil and Russia recorded sizable gains of 16.84% and 12.57%, respectively. Over the past year, emerging markets outperformed international developed markets by approximately 11%. Future expected returns for emerging markets still look relatively bright.

Commentary

Commentary

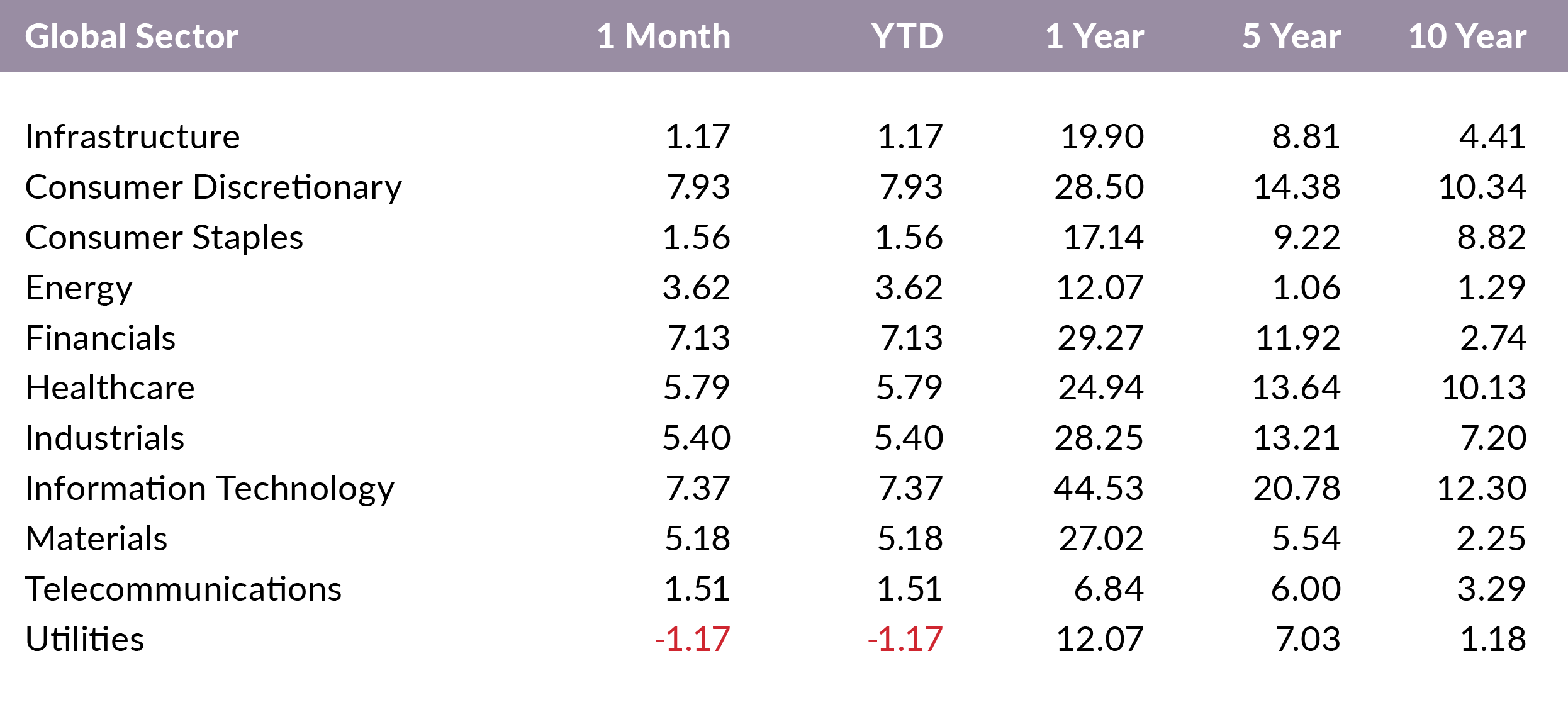

Consumer Discretionary Shines– Consumer discretionary and information technology posted the strongest global sector returns of 7.93% and 7.37%, respectively. Utilities was the only sector to drop in January. Macro trends have helped certain sectors more than others. Consumer discretionary has gotten a lift from this mature business cycle and the accompanying wealth effect felt by many people. Rising rates also tend to help financial firms.

Commentary

Commentary

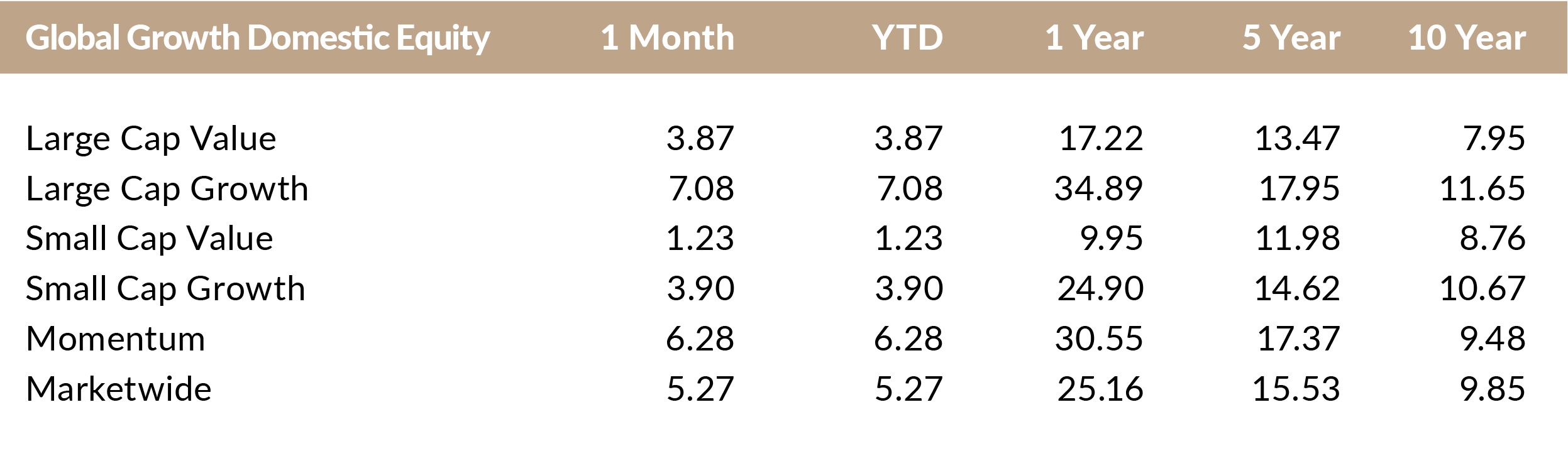

Momentum Picks Up– In January, growth outperformed value while momentum recorded a strong return of 6.28%. Given the U.S. is in the later stages of the business cycle, growth’s outperformance isn’t entirely unexpected, but investors with longer time horizons should still expect a value premium as history suggests.

Commentary

Commentary

Foreign Large-Cap Value Has Strong Month– In the international developed markets, large-cap value outperformed growth for the month. Small-cap growth outperformed small-cap value by 1.42%. Momentum posted a gain of 5.98%%. The outperformance of growth versus value is less drastic than the U.S. numbers.

Commentary

Commentary

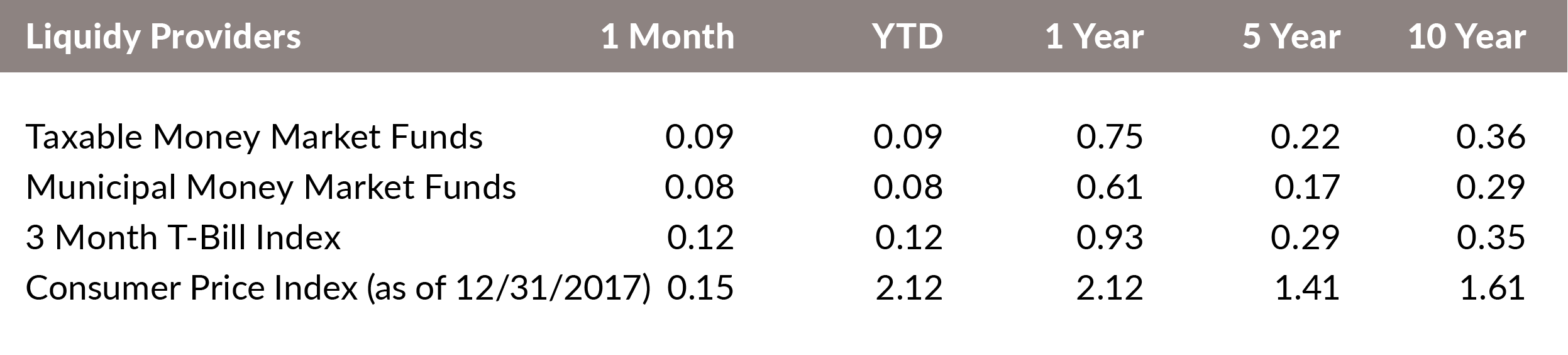

CPI Rises 2.12% in 2017– Both money market funds and T-Bills returned less than a percent over the past year. In 2017, the CPI increased by 2.12%. Investors may expect to see higher money market yields as the Fed continues to raise rates.

Commentary

Commentary

Deflationary Hedges Mostly Lower – The returns of deflationary hedges were mostly negative in January. Investors were rewarded for taking on credit risk as leveraged loans and high yield returned 0.96% and 0.64%, respectively. The global catastrophe bond index returned 1.33%. Traditional fixed income will face headwinds as central banks continue to tighten by raising rates or slowing their bond purchases.

Commentary

Commentary

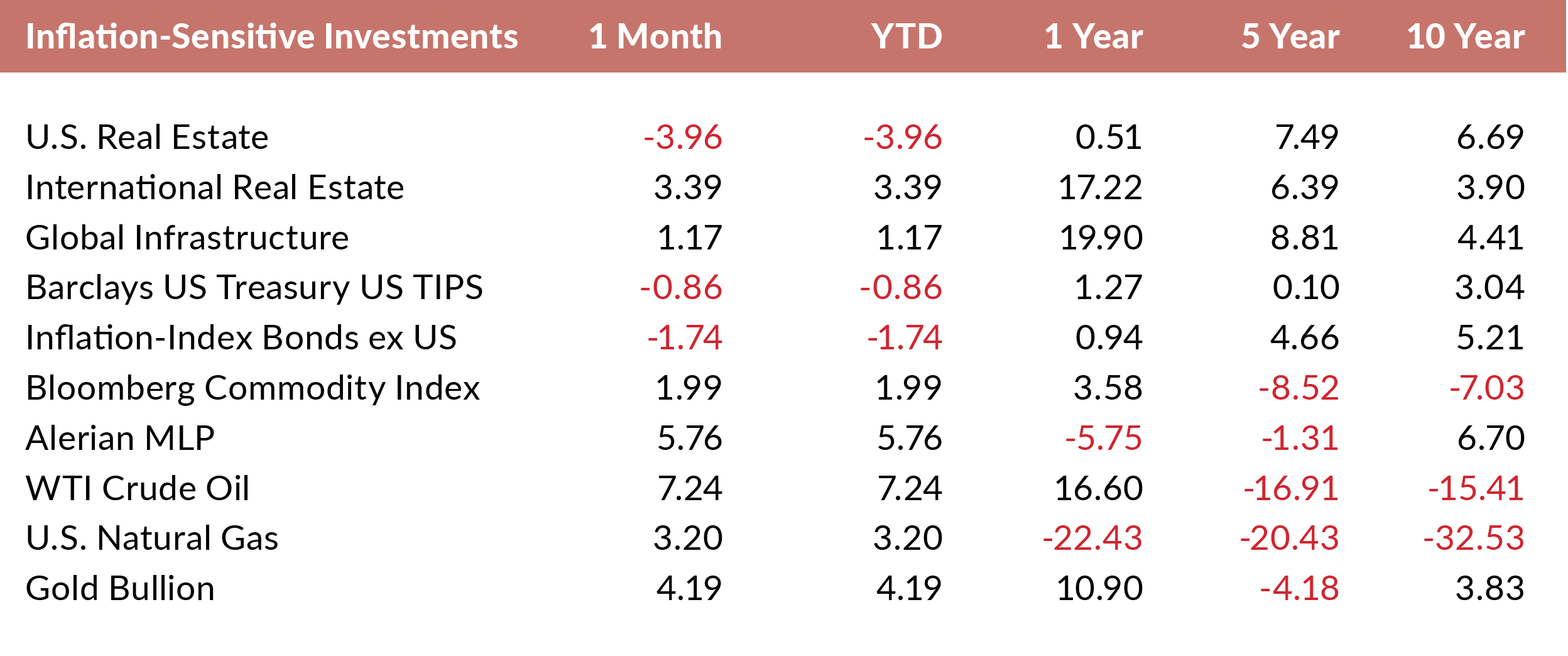

Energy Related Investments Record Monthly Gains– Inflation-sensitive investment returns were mostly positive in January. WTI Crude Oil and the Alerian MLP posted gains of 7.24% and 5.76%. U.S. real estate and inflation-indexed bonds were down for the month. Unexpected inflation is still a risk as the U.S. is in the later stages of the business cycle and the past quantitative easing by the major central banks has yet to produce many consequences.

Commentary

Commentary

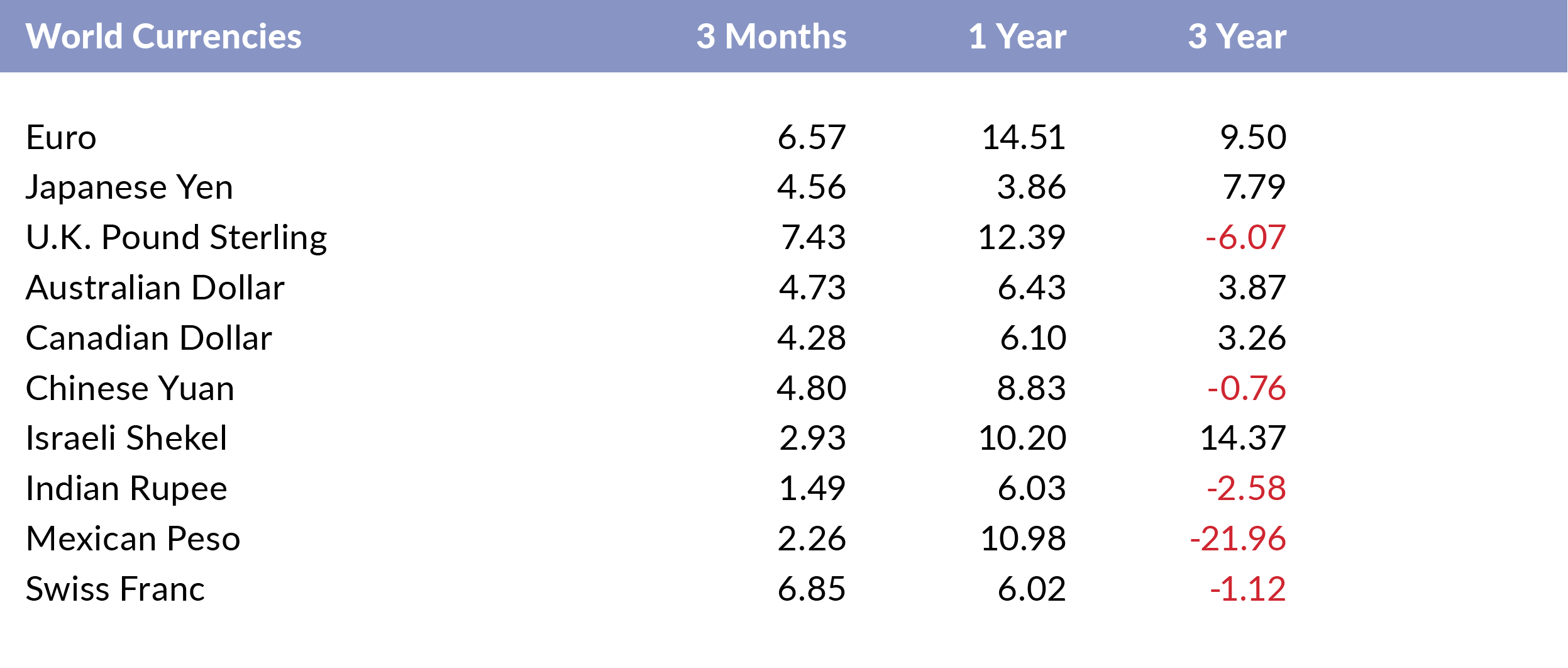

U.S. Dollar Depreciates Against Other Major Currencies– Over the past year, the U.S. Dollar depreciated against most other major currencies. The Euro and British Pound gained the most ground. The Mexican Peso and Israeli Shekel also had sizable appreciation against the U.S. Dollar.

[mk_fancy_text color=”#444444″ highlight_color=”#ffffff” highlight_opacity=”0.0″ size=”14″ line_height=”21″ font_weight=”inhert” margin_top=”0″ margin_bottom=”14″ font_family=”none” align=”left”]Disclosure: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Versant Capital Management, Inc.), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Versant Capital Management, Inc. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Versant Capital Management, Inc. is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Versant Capital Management, Inc. client, please remember to contact Versant Capital Management, Inc., in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Versant Capital Management, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request[/mk_fancy_text]