[vc_row][vc_column][vc_column_text responsive_align=”left”]

Cryptocurrency/Blockchain Technologies as an Investment

Why it’s a Speculative Market

Tyler J. Scott, Research Analyst

Extrinsic vs Intrinsic Value

Current cryptocurrency valuations are fueled by extrinsic valuations also known as speculation. Intrinsic valuation of a product or firm is a result of using, most commonly, discounted cash flow analysis to forecast future revenues and costs to produce guidance for the projected free cash flows.

The process of forecasting these revenues and costs is a result of past performance and forward-looking projections that are made within the context of a large set of known information. Cryptocurrencies and blockchain technologies have little to no past-performance and the set of known information on this space is incredibly nascent. This inherently means that even the most prudent investors are making frontier predictions about the adoption of these products and services. In many cases, these investors are not even attempting to make frontier predictions and are blindly assuming that current cryptocurrency valuations will continue to appreciate in value because everything the news cycle feeds them indicates that will be the case.

The real intrinsic value of cryptocurrencies will greatly depend on the future demand for the products/services they provide. A fair comparison would be Visa’s service offering to banks and consumers, of a centralized ledger to reconcile transactions made using Visa’s payment technology, charging a small fee for maintenance and execution of the technology. While some cryptocurrency/blockchain technologies may certainly evolve into meaningful businesses, most will not.

Regulatory Concerns

Even if we assume that we can accurately project the future cash flows that these products or services will produce, there is still significant regulatory/jurisdictional risk that needs to be mentioned. The fundamental idea of cryptocurrencies/blockchain technologies is that a system should be decentralized to use community and consensus to draw conclusions and execute accordingly. This is antithetical to the world of state governments and fiat currencies that rely on deeply centralized systems to facilitate the medium of exchange in any specific jurisdiction.

While some jurisdictions, such as Japan and Switzerland, seem to be ready to incorporate and legalize the use of these products/services in their economy, many are not and may never be. Until there is more consistent adoption amongst jurisdictions and a known regulatory framework globally, it is nearly impossible to identify the value of these products/services.

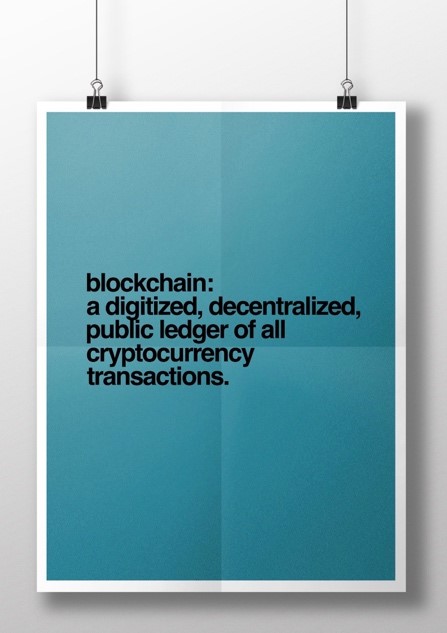

Cryptocurrencies vs Blockchain

There has been a lot of recent discussion about both cryptocurrency and blockchain technologies. The question that usually arises is, “What is the difference between the two and is one a better investment opportunity than the other?” The answer is that it is complicated and takes a deeper understanding of the full blockchain ecosystem to understand more clearly. Simply put, blockchain is the database technology that underpins cryptocurrencies. Unlike traditional databases, the blockchain is a distributed ledger with information not all controlled by one central database.

Bitcoin, the original cryptocurrency was built on this type of blockchain ledger to achieve the decentralized exchange that was the purpose of its development. Uniquely, bitcoin has written into its blockchain base layer protocol limitations to the mining of the cryptocurrency that eventually will result in the mining of bitcoin no longer being able to take place (creating scarcity). This was a result of bitcoin being developed in a way that mirrors aspects of gold and its ability to be a fungible store of value outside of fiat currencies. That isn’t to say that bitcoin has the same investment qualities as gold, rather, that bitcoin was written so that it could be potentially viewed in the same light as gold.

The issue for cryptocurrencies is that the process of “mining” them is essentially just the execution of calculations by computers to support and maintain the exchange of that respective cryptocurrency. This means that the entire mining process is based on code/protocols written by humans and can be changed if a majority-consensus of developers decide it is in their best interest.

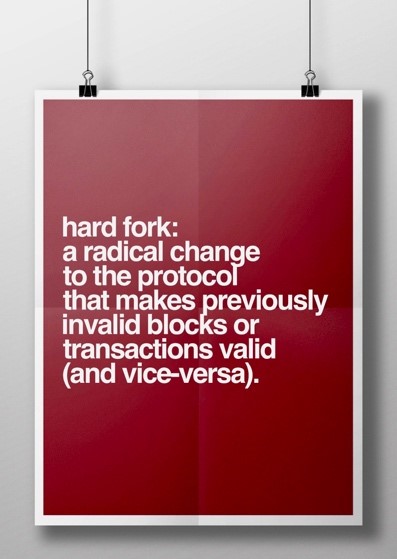

We have seen in the news that bitcoin’s hard fork has the potential to create a new bitcoin-based cryptocurrency that could either bolster the original bitcoin’s value or lower it, based on the blockchain developers’ perception of the decision to fork. All cryptocurrencies/blockchain technologies inevitably revolve around the use of expensive database systems with programmatic protocols.

Miners are incentivized to maintain these databases by being rewarded tokens for doing so. This offers execution of transactions amongst parties that find it difficult to resolve issues amongst themselves without having to seek out legal or other remedies. Instead, they rely on the developer network to address these issues through protocols. It is unclear how many use cases this would apply to, but it is most likely not as many as one would think, as many parties are able to come to a consensus without the need for legal help, etc. Why would you pay a development community tokens for managing your database if you are comfortable with your counterparty and have minimal concerns about their integrity/stewardship?

Current Trends and Investment Strategies

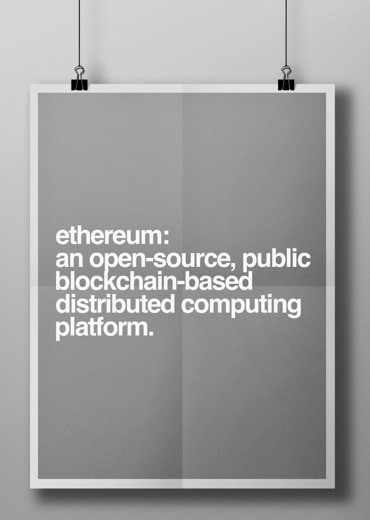

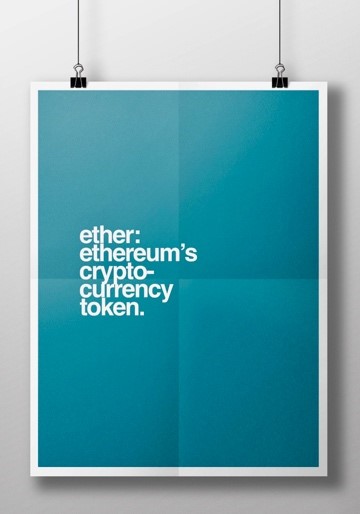

The application of blockchains – public or enterprise – will certainly continue to expand and there will be use cases that merit the use of this technology. What those will be and what cryptocurrencies/base layer protocols are used to facilitate these use cases is still highly uncertain at this time. Ethereum and its respective token, Ether, show how the blockchain/cryptocurrency valuations may be tied to these demands in the future.

Ethereum is a blockchain that allows for the execution of smart contracts that are programmatically tied to its base layer protocol. This means that as developers create Ethereum tools and consumers demand those tools, the value of its respective tokens should go up and down as a result of the forecasted supply and demand dynamics. However, given that any public or enterprise blockchain can be replicated, it seems naïve to expect that any given token will maintain its dominancy. It is likely that many tokens will be used independently of each other and compete for the demand of consumers over the intended use cases.

The current investable universe of cryptocurrencies/blockchain enterprises is very small. Most of what is mentioned in the news cycle has related to holding cryptocurrency portfolios in a digital wallet. Many blockchain startups have focused on providing this simple service as essentially a broker/custodian of cryptocurrencies. Currently, there are a small number of publically traded equities that invest directly in the mining of cryptocurrencies. These miners are investing in the commercial-scale mining of cryptocurrencies and are focused on minimizing operating costs and mining the most profitable cryptocurrencies at current prices. These firms act similarly to actual miners of physical commodities in relation to the structure of the business. However, the prices of the cryptocurrencies are subject to volatilities that are significantly higher than those for physical commodities.

The most diversified and forward-looking investments seem to be venture capital firms that are either taking part in this space (in addition to many other tech fields) or are solely focusing on blockchain as the entirety of their funds. These funds are investing in many aspects of the blockchain ecosystem and seem to be focused on investing in products/services that they feel strongly will merit the demand of consumers. There are even funds that are being created to make fiat investment funds (mutual funds, etc.) accessible by cryptocurrencies. Most of these are too fledgling to truly be considered an investment.

A Speculative Market

Cryptocurrencies and the blockchain technologies that support them have captured the attention of investors and consumers alike. Many would describe this enthusiasm as analogous to that of the dotcom bubble, where any product or service that relates to cryptocurrencies or blockchain technologies has been consistently rising in value at rates that have created enormous wealth for some. However, this appreciation does not seem to be tied to any specific fundamental analysis of the intrinsic value these products/services offer.

It will take time to fully understand how many use cases will be appropriate for these products/services. Until that point, the blockchain universe should be viewed as a speculative market and not something that can or should be recommended as an investment.

[mk_fancy_text color=”#444444″ highlight_color=”#ffffff” highlight_opacity=”0.0″ size=”14″ line_height=”21″ font_weight=”inhert” margin_top=”0″ margin_bottom=”14″ font_family=”none” align=”left”]Disclosure: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Versant Capital Management, Inc.), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Versant Capital Management, Inc. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Versant Capital Management, Inc. is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Versant Capital Management, Inc. client, please remember to contact Versant Capital Management, Inc., in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Versant Capital Management, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.[/mk_fancy_text][/vc_column_text][/vc_column][/vc_row]