[vc_row][vc_column][vc_column_text responsive_align=”left”]

MONTHLY MARKET REPORT: June 2018

Prepared by Brandon Yee, CFA, CAIA, and Thomas Connelly, CFA

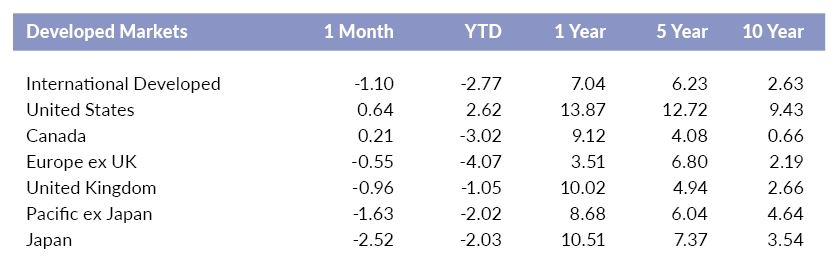

Developed Markets

Commentary

Developed Markets Fall– In the month of June, international developed stock markets in the aggregate fell by 1.10%. The U.S. and Canada recorded small gains of 0.64% and 0.21%, respectively. Developed markets, except the U.S., are slightly down for the year.

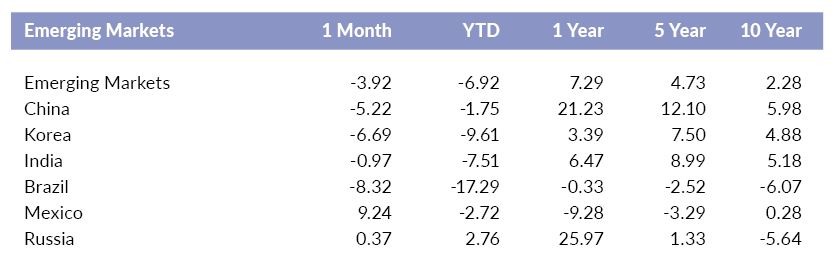

Emerging Markets

Commentary

Mexico Bounces Back– Broader emerging markets dropped 3.92% in June. Mexico and Russia posted gains of 9.24% and 0.37%, respectively. Brazil and Korea fell by 8.32% and 6.69%, respectively. Increased US dollar strength and trade tensions have caused higher volatility since many emerging markets are export-oriented. However, relative valuations still favor the developing nations.

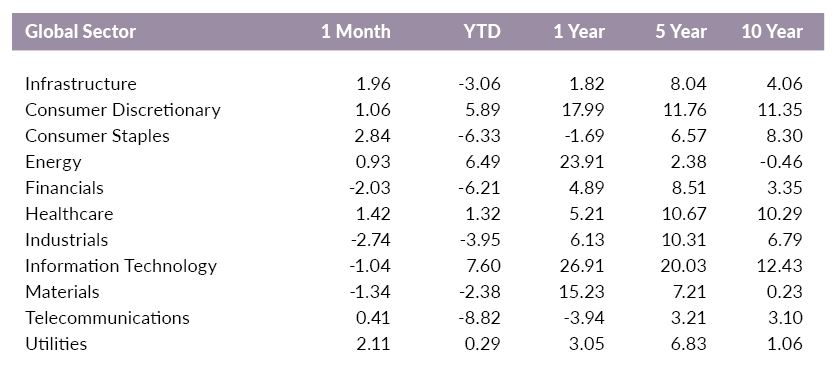

Global Sector

Commentary

Defensive Sectors Shine- Consumer staples and infrastructure recorded gains of 2.84% and 1.96%, respectively. Industrials and financials dropped the most in June, pulling back 2.74% and 2.03%, respectively. June returns favored the defensive sectors as investors reassessed the current market environment.

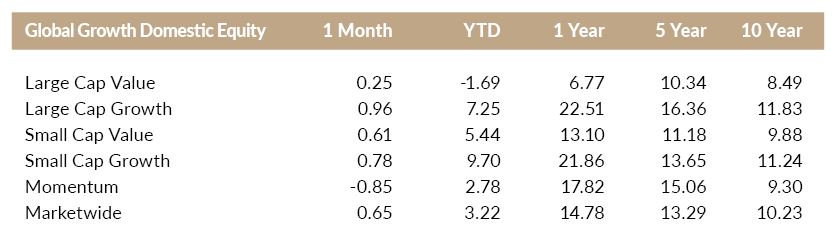

Domestic Equity Factors

Commentary

Growth Outperforms- In June, growth outperformed value. Momentum dropped by 0.85%. The size premium has been positive so far in 2018. Investing in smaller companies has historically compensated investors for taking on the added risk.

Foreign Equity Factors

Commentary

Small Cap Emerging Market Companies Tumble– In the international developed markets, growth outperformed value for the month. Momentum posted a loss of 1.57% and is flat for the year. Smaller emerging market companies underperformed their large cap counterparts.

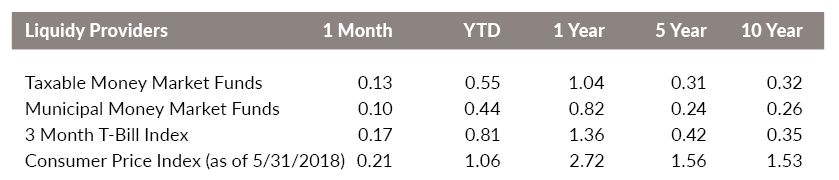

Liquidity Providers

Commentary

Savers Benefit from Rising Rates– Money market fund and T-Bill yields have steadily risen as the Fed continues to raise rates. The CPI increased by 2.72% year over year, above the Fed’s target rate of 2%. Increasing trade tensions could bring more inflation to the U.S.

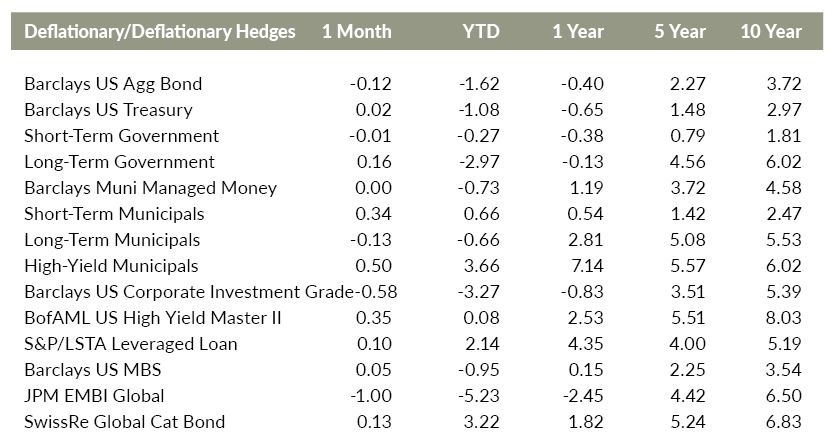

Disinflationary / Deflationary Hedges

Commentary

Fixed Income Mixed in June– The returns of deflationary hedges were mixed in June. High yield municipal bonds and high yield taxable bonds recorded gains of 0.50% and 0.35%, respectively. Emerging market bonds and investment grade corporate bonds fell. Traditional fixed income will face headwinds as central banks continue to tighten and rates rise.

Inflation-Sensitive Investments

Commentary

Oil Prices Rise – Inflation-sensitive investment returns were mixed for the month. Crude oil and U.S. real estate recorded gains of 8.85% and 4.24%, respectively. Commodities and gold bullion were down for the month. Dollar strengthening has been a headwind to gold’s return, but the metal may prove to be a valuable portfolio diversifier as the fiscal positions of many developed countries deteriorate.

World Currencies

Commentary

U.S. Dollar Appreciates– Over the past three months, the U.S. Dollar appreciated against most other major currencies. The Mexican Peso and British Pound dropped the most relative to the U.S. Dollar. Over the past year, the Euro and Chinese Yuan have strengthened moderately against the U.S. Dollar.

Brandon Yee, CFA, CAIA – Research Analyst

Brandon conducts investment due diligence for Versant Capital Management, and designs and implements tools and processes to support the firm’s research. His background in biology and finance help him to look at challenges from multiple angles, resulting in unique and well-rounded approaches and solutions.

[mk_fancy_text color=”#444444″ highlight_color=”#ffffff” highlight_opacity=”0.0″ size=”14″ line_height=”21″ font_weight=”inhert” margin_top=”0″ margin_bottom=”14″ font_family=”none” align=”left”]Disclosure: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Versant Capital Management, Inc.), or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from Versant Capital Management, Inc. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Versant Capital Management, Inc. is neither a law firm nor a certified public accounting firm and no portion of the article content should be construed as legal or accounting advice. If you are a Versant Capital Management, Inc. client, please remember to contact Versant Capital Management, Inc., in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Versant Capital Management, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.[/mk_fancy_text][/vc_column_text][/vc_column][/vc_row]