[vc_row][vc_column][vc_column_text]MONTHLY MARKET REPORT: March 2018

Prepared by Brandon Yee, CFA and Thomas Connelly, CFA

Commentary

Commentary

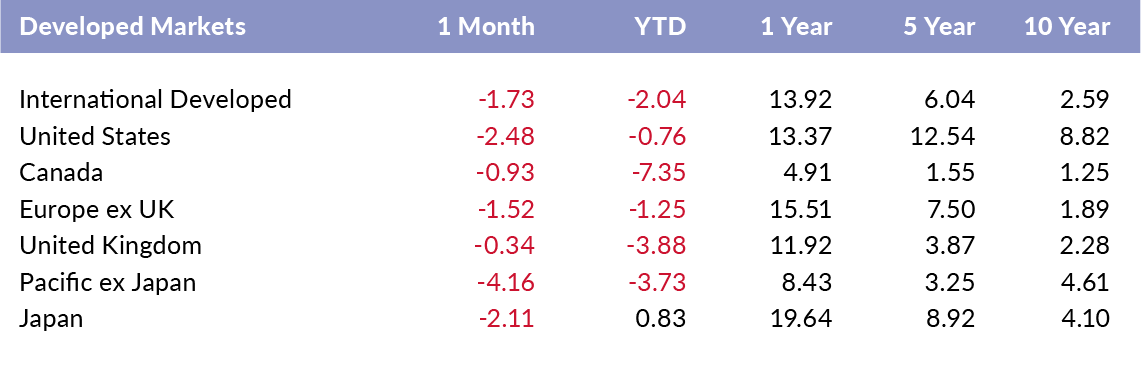

Developed Markets Sell Off– In the month of March, every major developed stock market fell. The UK and Canada recorded the strongest relative performance, losing less than other markets. The Pacific ex Japan region and the U.S. posted the largest losses of -4.16% and -2.48%, respectively. Japan is up 0.83% for the year. Trade tensions caused higher market volatility towards the end of March. Investors may face continued volatility if trade tensions increase.

Commentary

Commentary

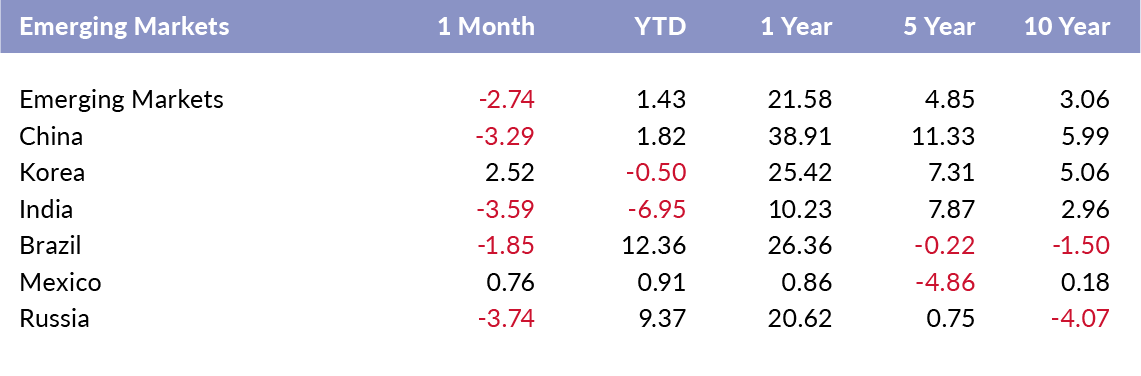

Emerging Markets Drop in March – Broader emerging markets dropped 2.74% in March. Korea and Mexico recorded strong returns of 2.52% and 0.76%, respectively. Russia and India fell the most in March. Emerging markets are up 1.43% for the year, with Brazil and Russia leading the way. Emerging markets have proven to be resilient even with the higher market volatility in developed markets.

Commentary

Commentary

Utilities Post Gains- Utilities and energy posted gains of 4.11% and 1.16%, respectively. Financials and materials dropped the most in March. Information technology pulled back, but the sector is still up 2.81% in 2018. In the volatile month of March, defensive sectors such as utilities and consumer staples held up better than their cyclical counterparts.

Commentary

Commentary

Growth Facing Headwinds- In March, value outperformed growth in the large cap space, but slightly underperformed among the small cap companies. Momentum dropped 2.40% for the month. Growth-oriented firms are still up in 2018, but may face headwinds if technology firms continue to face heightened pressure from investors and the current administration.

Commentary

Commentary

Momentum Strategies Fall– In the international developed markets, value underperformed growth for the month. Momentum posted a loss of 2.05%. Emerging small cap companies outperformed their large cap counterparts.

Commentary

Commentary

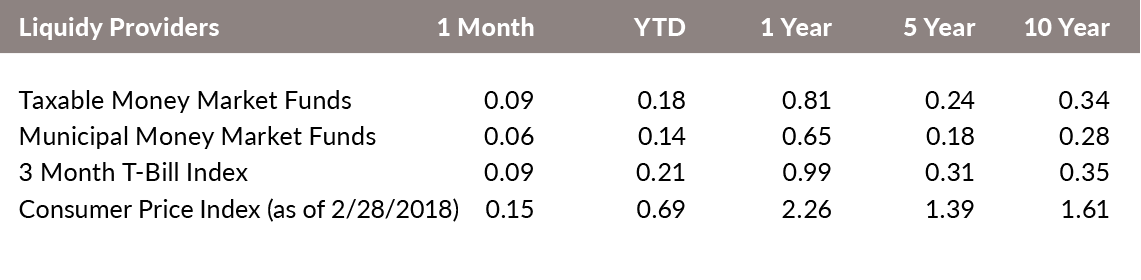

Rates Steadily Rising– Money market fund and T-Bill yields still trail the CPI, but savers may benefit more as the Fed continues to raise rates. The CPI increased by 0.69% through the end of February and increased 2.26% year over year. Increased trade tensions could bring more inflation to the U.S.

Commentary

Commentary

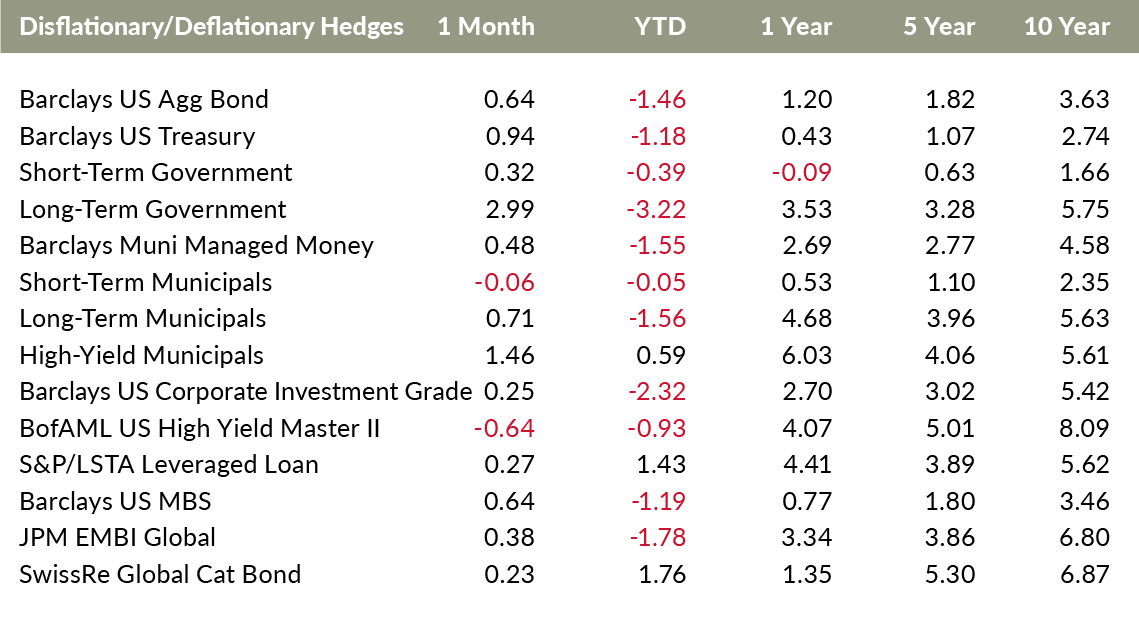

Deflationary Hedges Prove Valuable in March– The returns of deflationary hedges were mostly positive in March. Long-term government bonds and high-yield municipal bonds had the highest returns of 2.99% and 1.46%, respectively. High-yield corporates and short-term municipal bonds fell. Traditional fixed income will face headwinds as central banks continue to tighten.

Commentary

Commentary

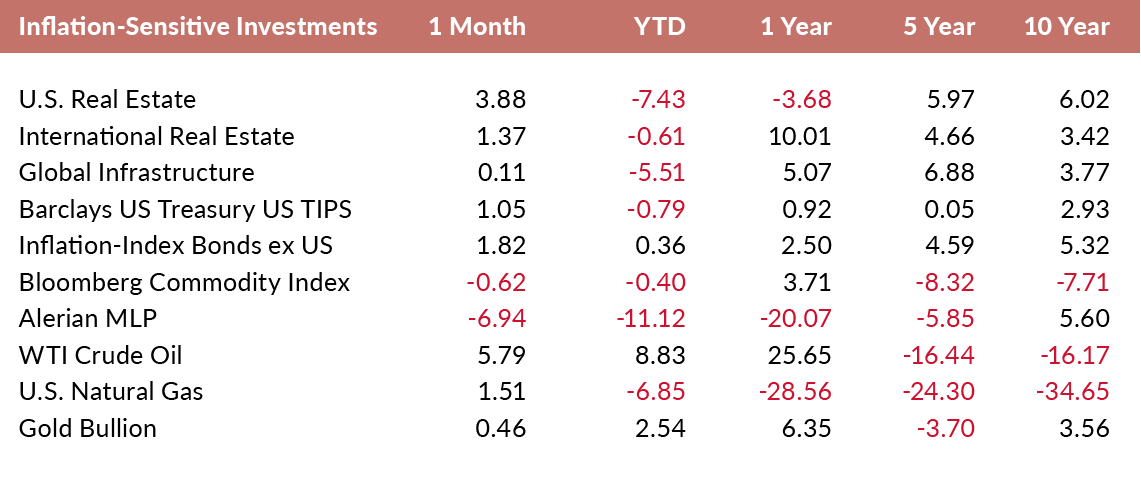

MLPs Continue Slide– Inflation-sensitive investment returns were mostly higher in March. Crude oil and U.S. real estate recorded gains of 5.79% and 3.88%, respectively. The Alerion MLP was sharply lower, dropping approximately 7% for the month and 20% over the past year. Unexpected inflation is still a risk as the U.S. is in the later stages of the business cycle and past quantitative easing by the major central banks has yet to produce many consequences.

Commentary

Commentary

Japanese Yen Appreciates– Over the past three months, the Mexican Peso and Japanese Yen gained the most ground against the U.S. Dollar. The Canadian Dollar and Indian Rupee dropped the most relative to the U.S. Dollar during the same time period. Over the past year, the Euro has strengthened considerably.

[mk_fancy_text color=”#444444″ highlight_color=”#ffffff” highlight_opacity=”0.0″ size=”14″ line_height=”21″ font_weight=”inhert” margin_top=”0″ margin_bottom=”14″ font_family=”none” align=”left”]Disclosure: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Versant Capital Management, Inc.), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Versant Capital Management, Inc. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Versant Capital Management, Inc. is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Versant Capital Management, Inc. client, please remember to contact Versant Capital Management, Inc., in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Versant Capital Management, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.[/mk_fancy_text][/vc_column_text][/vc_column][/vc_row]